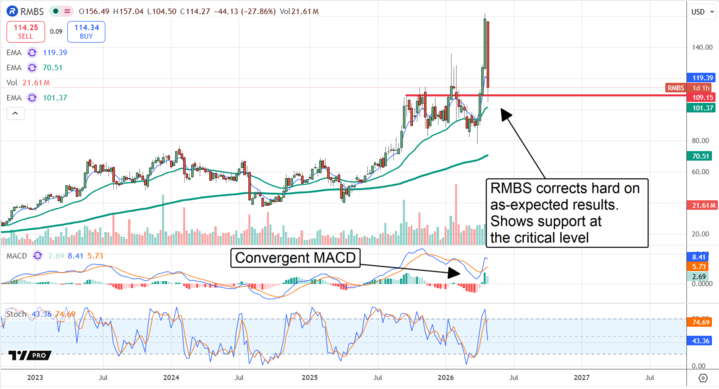

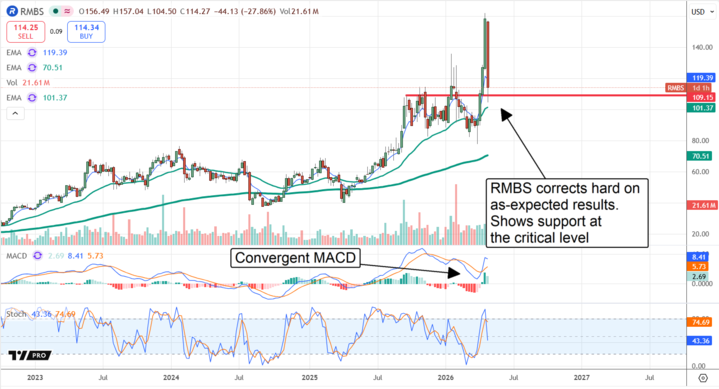

Rambus’ (NASDAQ: RMBS) stock price took investors on a wild ride in April, surging to fresh highs then collapsing in the wake of its earnings release. The candle formed in late April is scary, a large red candle nearly engulfing the prior two weeks, but this is one bear investors will want to cuddle. While the late April price action raises some questions, the implications are clear. Rambus is well-positioned within the AI world, has a long runway for growth, and the sell-off was and is a buying opportunity

Rambus Had a High Bar to Beat: As Expected Just Wasn’t Good Enough

Rambus’ stock price decline was centered on the price action prior to its Q1 earnings release. There was a high expectation for shockingly strong results, given the GPU and datacenter demand.

Once primarily the licenser of intellectual property (IP), the company now designs and markets a widening range of memory interface products. These are not merely the connections between memory chips, but advanced semiconductor technology that enables the efficient operation of GPUs, clusters and data centers.

In the end, the results affirmed the company’s position, with product revenue growing to $88 million, accounting for nearly 50% of sales, and management highlighting the long-term potential. In management’s view, it is the rise of agentic workflows and inference that drives demand for Rambus’ products, a much larger market than the infrastructure side and one even earlier in its evolution. The likely outcome is that RMBS will continue to drive growth in the long term, potentially accelerating alongside AI adoption over the coming years.

Misplaced DRAM Concerns: Acceleration Coming in 2027

Among the catalysts for Rambus’ stock price decline was a downgrade from Robert W. Baird. Analysts at the firm cut the rating to Hold, leaving the price target unchanged, citing concern over DRAM supply. The company cited shortages as hindering their growth, but this is a near-term phenomenon.

Companies such as Micron Technology (NASDAQ: MU) (and all other DRAM manufacturers) are actively ramping production and capacity, with significant improvement in DRAM availability expected by late 2027. In this scenario, Rambus may struggle to accelerate growth in the near term, but business remains assured, and the long-term outlook remains robust. In this scenario, not only is there an opportunity for this company to surprise in the upcoming quarters, but also a business acceleration tied to DRAM supply improvements.

Analysts, in General, Liked What They Saw in Rambus’ Earnings Report

Robert W. Baird’s downgrade was not without cause, but it is an outlier.

The bulk of responses increased and reaffirmed price targets, leading to an above-consensus price point, including a new high target of $172.

The data tracked by MarketBeat reveals a moderate-conviction Moderate Buy consensus among 10 analysts with potential for 15% upside from the critical support level and an uptrend in the price targets.

The consensus of fresh targets, including Baird’s reaffirmed $120, places this market even higher, near $145, $15 above the broader consensus and on track to hit fresh highs.

The Price Action Is Kinda Bullish, Believe It or Not

Rambus’ stock price decline suggests a deeper pullback is possible, but many factors, including price action, critical targets, and the MACD indicator, suggest otherwise. To begin, RMBS stock advanced sharply from its March low, accelerating over four weeks to set a new high, breaking above the DotCom high for the first time in over two decades. The price action formed Three, and then Four White Soldiers, a sign of a strengthening market with the capacity to continue higher. Regarding the price pullback, it shows support at the critical prior highs and is likely a strong level, given the ramp in trading volume over the past year.

The MACD indicator is the operative signal in this case. The MACD is a measure of market momentum and affirms strengthening through convergence. The MACD peak set in April converges with the fresh high and is an Extreme Peak, as it is the largest momentum swing on record. The implication is that this market will retest the recent high, at least, and will probably set a fresh high. The question is whether the fresh high is sustained and if even higher highs will come.

Rambus Results Weren’t Bad, No Reason to Shed 25% Here

Rambus’ results were not bad, far from it, merely less than what the market had hoped. Revenue grew by a high single-digit amount, earnings by a slightly lower amount, and cash from ops by 15%. The net result was an increase in shareholder equity and the capacity to continue executing the strategy. That is IP development and, now, sales associated with it. The catalysts in 2026 include the expansion of the product line, with the launch of SOCAMM2 products, and the shift from DDR5 Gen2 to Gen3.

Before you make your next trade, you’ll want to hear this.

MarketBeat keeps track of Wall Street’s top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on… and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now…

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.