As the Q1 earnings season progresses, Texas Instruments TXN) and IBM IBM) have provided a pivotal moment that has reconfirmed market sentiment more than reshaped it.

The reconfirmation is that semiconductor companies are still prime investments right now, thanks to AI data center expansion, but that AI may start to eat the lunch of software companies, and the segments of tech giants exposed to or dependent on software operations.

Texas Instruments may not be at the forefront of investors’ minds regarding the AI data center boom, but its Q1 results showed it’s a promising player in the landscape. On the other hand, there are growing concerns that IBM’s software segment could come under pressure despite posting favorable quarterly results as well.

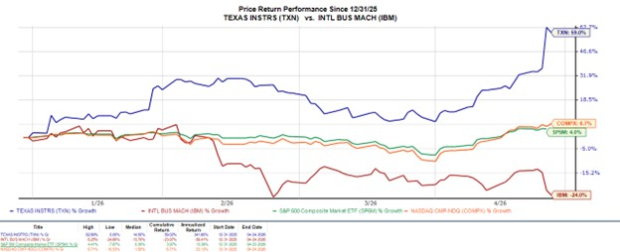

Following their Q1 reports on Wednesday, TXN shares have spiked to a new 52-week high and kept the rally going among chip stocks, with IBM falling near a one-year low and reigniting a pullback in software stocks amid AI disruption fears.

Image Source: Zacks Investment Research

Texas Instruments’ Data Center Expansion

Notably, Texas Instruments’ data center business focuses on supplying the power, signal-conditioning, and interface chips that keep AI data centers running. Because Texas Instruments sells analog and power-management components rather than full systems, its chips are purchased through original equipment manufacturers (OEMs) and server manufacturers, making customer identification indirect.

That said, its largest buyers are thought to be the major hyperscalers such as Amazon AMZN), Microsoft MSFT), Alphabet GOOGL), and Meta Platforms META) — all of which operate massive data center footprints across the United States.

Keeping this in mind, Texas Instruments reported that its data center segment revenue soared 90% year over year during Q1 and grew more than 25% sequentially.

This helped drive Q1 sales up 19% YoY to $4.82 billion, eclipsing estimates of $4.51 billion by nearly 7%.

Image Source: Zacks Investment Research

Taking advantage of the surging data center demand that has boosted its analog and embedded processing businesses, Texas Instruments’ Q1 earnings spiked 31% YoY to $1.68 per share and came in 22% above EPS expectations of $1.37.

Image Source: Zacks Investment Research

Why IBM’s Slower Software Growth Sparked Concerns

Despite concerns of slower software segment growth, IBM was also able to post solid Q1 results with quarterly sales increasing 9% YoY to $15.91 billion and EPS rising 19% to $1.91. These figures topped sales and EPS estimates by 1% and 5%, respectively.

Image Source: Zacks Investment Research

Software revenue grew 11% YoY, but this was down from 14% growth in the previous quarter, marking a clear deceleration after delivering accelerating sequential growth for several quarters.

It’s noteworthy that IBM’s software segment consists of four major operational pillars: Hybrid Platform & Solutions, Red Hat (open source software platform), Transaction Processing, and AI Data Automation Products. Together, they form the core of IBM’s recurring-revenue, which is why the market is concerned about the slowdown.

Analysts have noted that AI-driven competitive pressure and emerging generative AI tools could erode demand for IBM’s traditional software offerings. The disruptors include AI-native tools like Anthropic’s COBOL-modernization AI.

Conclusion & Strategic Thoughts

Outside of the nuances in their quarterly reports, Texas Instruments ignited favorable momentum by raising its revenue and EPS outlook for Q2, while IBM underwhelmed investors by leaving its full-year guidance unchanged and citing geopolitical and macroeconomic uncertainties as reasons for caution.

More upside does look apparent for semiconductor leaders like Texas Instruments, with TXN currently sporting a Zacks Rank #2 (Buy) based on a trend of positive EPS revisions.

IBM stock currently lands a Zacks Rank #3 (Hold) as a steady growth narrative is still there, although its EPS revisions have started to trend lower in the last 30 days. This pattern has been seen across many software stocks and those with exposure to the software as a service (SaaS) realm. However, the reignited selloff in the space could create longer-term opportunities if fears of AI disruptions become overdone, especially for prominent companies like IBM that have a variety of global business services and solutions, including hardware offerings.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Texas Instruments Incorporated (TXN) : Free Stock Analysis Report

International Business Machines Corporation (IBM) : Free Stock Analysis Report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Meta Platforms, Inc. (META) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.