Guidewire Software, Inc. GWRE is benefiting from insurers’ shift to cloud-based core systems, with recurring revenue growth and better profitability supporting the investment case.

The stock’s setup is still balanced. Large-deal timing, services mix, rising costs and the need to scale newer AI products without adding complexity remain key offsets.

Why GWRE Still Centers on Cloud Conversion

Guidewire serves property and casualty insurers with software for core operations, digital engagement, analytics, machine learning and AI. Its main cloud offerings include InsuranceSuite Cloud and InsuranceNow, both central to insurer modernization projects.

Cloud migration remains the main growth engine. In third-quarter fiscal 2026, Guidewire closed 11 cloud deals, including two net-new core system wins. Wins included a seven-year extension and DWP expansion with Auto Club of Southern California, a strategic net-new win with Bradesco Seguros in Brazil and selections by insurers in the United Kingdom and the United States.

SAP SE SAP is relevant to this discussion because SAP offers insurance software solutions for data-driven decisions, AI and compliance needs. Salesforce, Inc. CRM also fits the broader software context through its financial-services software and CRM offerings for customer engagement

How Guidewire Is Turning ARR Into Visibility

Annual recurring revenue remains one of the clearest measures of Guidewire’s cloud transition. ARR ended the third quarter at $1.147 billion, up more than 19% year over year.

Management maintained fiscal 2026 ARR guidance of $1.229-$1.237 billion, implying 18%-19% year-over-year growth. Fully ramped ARR continued to grow faster than reported ARR, giving investors a better view of contract value that has not yet fully flowed into reported ARR.

Where GWRE Is Finding Margin Improvement

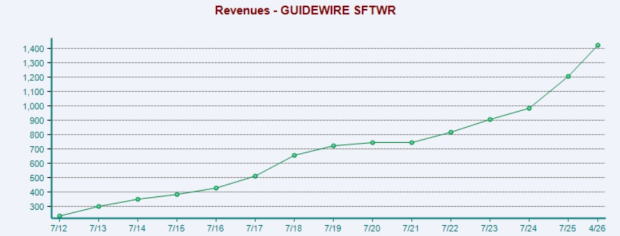

Subscription and support revenue is now doing more of the heavy lifting. In the fiscal third quarter, subscription and support revenues rose 34.6% year over year to $244.7 million, representing 65.7% of total revenues.

Image Source: Zacks Investment Research

Profitability is improving with scale. Non-GAAP subscription and support gross margin increased to 74% from 71% a year earlier, while overall non-GAAP gross margin expanded to 66.4% from 65.5%. Non-GAAP operating income rose to $77.8 million from $46.1 million in the year-ago quarter.

What Guidewire Must Prove on New Products

ProNavigator and PricingCenter are becoming the next layer of the story. Guidewire completed five ProNavigator deals in the third quarter as insurers looked to add AI-driven knowledge and workflow automation to insurance operations.

PricingCenter also gained traction, with three wins, including insurers in Sweden and Poland and the first U.S. win at Oklahoma Farm Bureau. These products can deepen customer relationships beyond core systems, but Guidewire still must scale them without adding delivery complexity or weakening economics.

How Zacks Signals Fit GWRE’s Balanced Setup

The bottom line on GWRE is that the company is executing well where investors need it most: cloud adoption, ARR expansion and margin improvement. At the same time, the stock’s outlook is not without friction, as large cloud deals can shift between quarters and newer offerings such as ProNavigator and PricingCenter still need to scale efficiently.

GWRE currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

GWRE has a Value Score of F, Growth Score of B, Momentum Score of F and VGM Score of D. The Growth Score reflects the company’s improving revenue profile, while weaker value and momentum marks suggest investors may want to watch execution, valuation and deal timing closely before taking a more aggressive stance.

For now, Guidewire’s cloud transition remains the core reason to stay engaged with the story. The next test is whether the company can convert its expanding platform, AI tools and pricing products into durable ARR growth without sacrificing the margin progress that has made the investment case more credible.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Salesforce, Inc. (CRM) : Free Stock Analysis Report

SAP SE (SAP) : Free Stock Analysis Report

Guidewire Software, Inc. (GWRE) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.