Allegro MicroSystems, Inc. ALGM has rebounded sharply as revenue growth, earnings leverage and end-market demand have improved. The setup is no longer just about recovery. It is about whether the next phase can justify a richer multiple.

The stock’s fundamentals look stronger, but the valuation already reflects a better story. That makes execution in margins, automotive growth and newer industrial markets the key issue for investors.

ALGM Growth Metrics Support the Bull Case

Fiscal 2026 showed a clear rebound. Revenues rose 22.8% year over year to $890.1 million, while non-GAAP earnings per share more than doubled to 54 cents from 24 cents.

Momentum also held into the fiscal fourth quarter. Sales increased 26.1% year over year to $243.2 million, and management guided first-quarter fiscal 2027 revenues to $245-$255 million. At the midpoint, that implies 23% year-over-year growth.

The more important point is earnings scalability. Earnings grew much faster than sales in fiscal 2026, helped by operating leverage and stronger demand across Focus Auto, Data Center and Industrial and Other markets.

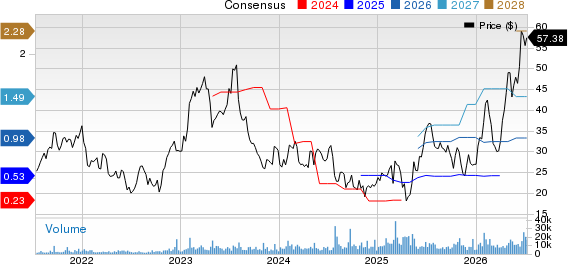

Allegro MicroSystems, Inc. Price and Consensus

Allegro MicroSystems, Inc. price-consensus-chart | Allegro MicroSystems, Inc. Quote

Why Allegro’s Margin Story Matters Most

Margin recovery is central to the buy case because Allegro’s sales growth is already visible. Non-GAAP gross margin reached 50% in the fiscal fourth quarter, up from 45.6% in the year-ago period.

The company expects non-GAAP gross margin of 50%-51% for the first quarter of fiscal 2027. Its longer-term target remains above 55%, supported by operating leverage, product innovation, cost reductions and manufacturing efficiencies.

That path is not automatic. Pricing pressure, average selling price declines and input-cost inflation, including gold and energy costs, remain constraints. Margin expansion may therefore come in stages rather than in a straight line.

Allegro’s Valuation Leaves Less Room for Error

The main caution is price. ALGM traded at 51.13X forward 12-month earnings, above 32.39X for the Zacks sub-industry, 24.53X for the Zacks sector and 21.03X for the S&P 500.

The 6-12 month price target of $61 also implies only modest upside from the cited share price of $57.38. That does not negate the fundamental improvement, but it reduces the margin of safety after a major rally.

Investors can also compare ALGM with Ichor Holdings, Ltd. ICHR and Nova Ltd. NVMI, both listed among its industry peers. These names give investors additional reference points within the Electronics – Semiconductors group when weighing valuation and momentum.

ALGM Risks Could Limit Further Upside

Automotive remains the largest exposure, accounting for roughly 71% of fiscal 2026 revenue. That concentration leaves Allegro sensitive to global vehicle production, electric vehicle adoption, advanced driver assistance system deployment and customer inventory cycles.

Newer growth markets also require execution. AI data centers and robotics are attractive, but customer qualification, design wins and product adoption still matter before those opportunities can fully scale.

Supply risk is another factor. Allegro relies on third-party wafer foundries, external assembly and testing partners and manufacturing operations in the Philippines. Trade restrictions, tariffs, geopolitical issues and macro weakness could pressure both revenues and margins.

How Allegro’s Ratings Frame the Setup

The bottom line is that ALGM looks fundamentally stronger, but not obviously cheap after its run. Growth, earnings leverage and margin recovery support the bull case, while valuation and execution risk argue for selectivity.

The stock currently carries a Zacks Rank #2 (Buy). That rank is designed for a one-to-three-month horizon and reflects favorable near-term earnings estimate characteristics. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

ALGM also has a Growth Score of A and a Momentum Score of A, which point to attractive growth and price-performance characteristics. Its Value Score of F explains the valuation concern, while the VGM Score of B keeps the overall style profile constructive but mixed.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Allegro MicroSystems, Inc. (ALGM) : Free Stock Analysis Report

Nova Ltd. (NVMI) : Free Stock Analysis Report

Ichor Holdings, Ltd. (ICHR) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.