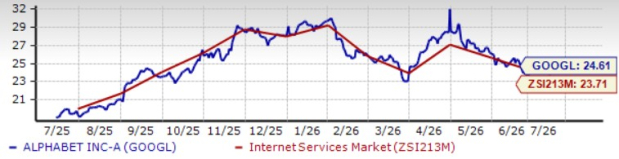

Alphabet GOOGL shares are overvalued, as suggested by a Value Score of D. The GOOGL stock is trading at a forward 12-month price/earnings (P/E) of 24.61X, a premium compared with the Zacks Internet Services industry’s 23.71X and broader Zacks Computer & Technology sector’s 24.27X.

Alphabet shares are trading at a premium compared with Microsoft MSFT, shares of which are trading at a P/E multiple of 19.82. However, GOOGL shares are trading at a lower multiple compared with Apple’s AAPL 33.51 and Amazon’s AMZN 25.98.

GOOGL Stock’s Valuation

Image Source: Zacks Investment Research

Is Alphabet worth buying at current prices? Let’s dig deep to find out.

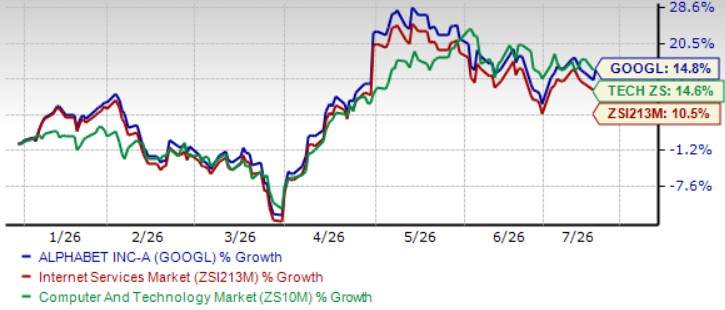

GOOGL Up a Modest 15% YTD: What’s Plaguing the Stock?

Alphabet shares have risen a modest 14.8% year to date (YTD), slightly better than the broader sector’s return of 14.6% and the industry’s 10.5%. GOOGL’s huge capital expenditure — between $180 billion and $190 billion — roughly double 2025’s level, with spending expected to rise further in 2027, has spooked investors. Alphabet nearly doubled first-quarter 2026 capital expenditure to $35.7 billion, with most spending directed toward AI infrastructure, including servers, data centers and networking equipment. The investment materially reduced quarterly free cash flow and has raised concerns that elevated AI spending could persist for several years.

GOOGL Stock’s Price Performance

Image Source: Zacks Investment Research

Alphabet’s prospects are suffering from stiff competition from the likes of Microsoft-backed OpenAI, Amazon, Anthropic and Meta across foundation models, enterprise AI, cloud infrastructure and AI assistants. The company’s heavy investments in talent hiring, GPUs, TPUs and model development are expected to keep margins under. Alphabet has also highlighted higher research & development as well as marketing expenses driven by AI investments and Gemini adoption, in this regard.

Alphabet is facing stiff competition in the cloud computing space from Microsoft and Amazon. According to Synergy Research Group’s first-quarter 2026 data, Amazon maintained a strong lead in the market, though Microsoft and Alphabet’s Google continued to achieve substantially higher growth rates. Amazon, Microsoft and Alphabet’s market share were roughly 28%, 21% and 14%, respectively. In the search domain, Google continues to dominate with a roughly 91.27% share, followed by Microsoft’s Bing, with a 4.68% share, per the latest data from StatCounter. In the consumer technology market, Alphabet faces stiff competition from Apple.

GOOGL’s search monetization policy has been put under scrutiny by investors. Although AI Overviews and AI Mode are boosting user engagement and search queries reached all-time highs, investors remain cautious about whether conversational AI can ultimately generate advertising revenues comparable to traditional search. Alphabet is still testing new AI-native advertising formats, leaving long-term monetization questions unresolved.

AI Push Boosts GOOGL’s Search & Cloud Business

Alphabet’s prospects are increasingly driven by AI, which is no longer a standalone initiative. AI is becoming the core growth engine across Search, Cloud, subscriptions, advertising, and emerging businesses. AI-powered features are being embedded across Search, YouTube, Chrome, Workspace and Google One subscriptions. First-party models now process more than 16 billion tokens per minute, paid subscriptions reached about 350 million, and Gemini adoption continues expanding across Search, Workspace, Chrome and consumer AI offerings.

Alphabet sees AI as creating an “expansionary moment” for Search rather than disrupting it. Management noted that AI-powered features are increasing engagement and driving search queries to all-time highs, similar to the growth acceleration created by the transition to mobile. Alphabet has also reduced AI response costs by more than 30% since upgrading to Gemini 3, improving future economics. AI also improves advertising effectiveness through a better understanding of user intent, allowing GOOGL to monetize longer and more complex searches while improving advertiser ROI.

Google Cloud is one of the clearest beneficiaries of AI adoption. Management emphasized that Enterprise AI Solutions have become the Cloud’s primary growth driver, with 75% of Cloud customers now using Google’s AI products. Cloud backlog nearly doubled sequentially to more than $460 billion in the first quarter of 2026, reflecting exceptional enterprise AI demand and providing significant revenue visibility. Alphabet’s ability to provide infrastructure, models, security and productivity tools through a single integrated platform positions Google Cloud to capture growing enterprise AI spending.

Strong enterprise adoption of AI bodes well for GOOGL’s prospects. In the first quarter of 2026, Gemini Enterprise’s paid monthly active users grew 40% sequentially, enterprise AI products grew nearly 800% year over year, customer acquisition doubled, and Google signed multiple $1 billion-plus AI deals. This suggests AI is evolving into a meaningful recurring enterprise software business for Alphabet.

2026 Earnings Estimate Revisions Positive for GOOGL Stock

The Zacks Consensus Estimate for 2026 earnings is pegged at $14.32 per share, up by a couple of cents over the past 30 days, indicating 32.47% growth from the figure reported in 2025. The consensus mark for 2026 revenues is pegged at $423.63 billion, indicating 23.54% year-over-year growth.

Alphabet Inc. Price and Consensus

Alphabet Inc. price-consensus-chart | Alphabet Inc. Quote

The consensus mark for second-quarter 2026 earnings is pegged at $2.86 per share, unchanged over the past 30 days, suggesting 23.81% year-over-year growth. The Zacks Consensus Estimate for second-quarter 2026 revenues is pegged at $101.22 billion, implying 23.86% year-over-year growth.

Here’s Why GOOGL Stock is a Buy Right Now

Alphabet’s long-term investment case remains compelling and justifies a premium valuation. The company continues to strengthen its leadership across Search, Cloud and digital advertising while rapidly transforming AI into a powerful growth engine spanning consumer and enterprise markets. Surging Cloud backlog, accelerating Gemini adoption, improving AI economics and positive earnings estimate revisions underscore the strength of its execution. As AI investments increasingly translate into higher revenue, deeper customer engagement and expanding monetization opportunities, Alphabet appears well-positioned to deliver sustained growth.

Alphabet currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA’s enormous potential back in 2016. Now, he has keyed in on what could be “the next big thing” in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.