As all three major indexes dipped into bear territory in 2022, investors have been anxiously pondering the inevitable: When will the next bull market make its grand entrance?

While pinpointing the advent of a bull market with unwavering precision is unattainable, there are a couple of reasons to hold onto hope for a bullish upswing.

Firstly, history instructs us that bear markets unfailingly precede bull markets, signifying that downtimes are transient. Secondly, scrutiny of historical data imparts an optimistic outlook on the Nasdaq Composite‘s potential to surge higher in 2024. Last year, the index skyrocketed by 43%, outperforming both the Dow Jones Industrial Average and the S&P 500, which posted gains of 13% and 24%, respectively. A retrospective examination of the Nasdaq’s performance reveals that after every year of rebounding from a bear market, the index has ascended during the subsequent year.

After each annual loss of over 10%, the Nasdaq subsequently experienced an average surge of 56% over the following two years. This historical trend signals ample potential for the Nasdaq to make significant strides this year, making the present an opportune moment to invest in high-quality growth stocks. These stocks are distinguished by their consistent capability to augment earnings over time, and they hold steadfast long-term prospects. By acquiring shares of such companies, it is plausible to achieve both short-term gains and sustained success. Here, we present two certainty-backed growth stocks that warrant immediate consideration.

Image source: Getty Images.

First Pick: Apple

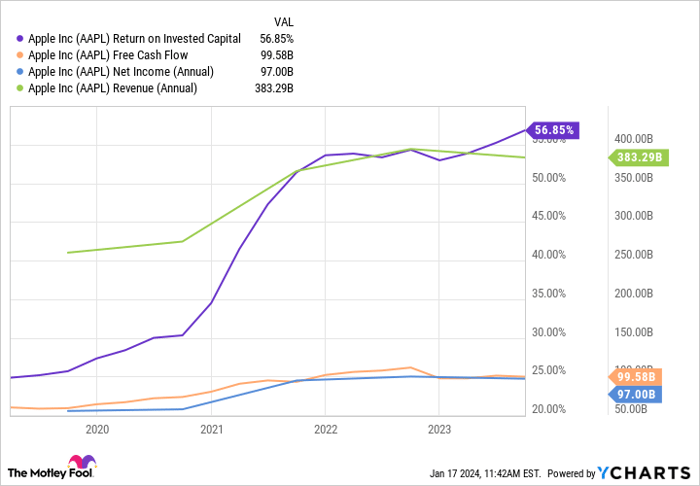

Apple (NASDAQ: AAPL) has consistently witnessed soaring revenue, profits, and other key metrics such as free cash flow and return on invested capital. This affirms the tech behemoth’s unwavering ability to consistently translate escalating revenue into profits and execute astute investment decisions.

AAPL Return on Invested Capital data by YCharts.

The resultant surge in share price has propelled the company to a market value exceeding $2.8 trillion. Evidently, Apple boasts a track record of triumphant endeavors.

This impressive feat is attributable to the company’s robust brand prowess. Customers consistently gravitate back to indulge in the latest iPhone or Mac, displaying resistance to being swayed by rival offerings. This resilience represents a moat, or competitive advantage, that is poised to perpetuate momentum.

Beyond safeguarding its existing customer base, Apple continues to expand its following. For instance, in the most recent quarter, half of the purchasers of Mac and iPad were new to those product lines. Furthermore, Apple persists in its trailblazing endeavors, with the imminent launch of its latest offering, the Apple Vision Pro spatial computer, slated for early next month.

Presently, over 2 billion individuals globally utilize Apple devices, paving the way for a discussion on Apple’s next substantial growth catalyst. This refers to the suite of services Apple avails to these device users, ranging from cloud storage to digital content. In the latest quarter, services revenue surged to a record high and is destined to continue flourishing, owing to the mammoth and expanding user base of Apple. Furthermore, the margins from Apple’s services substantially exceed those from its products — 70% versus 36% in the recent quarter.

These factors collectively indicate that despite amassing a 48% upsurge last year, Apple possesses untapped potential. In a market that favors growth, this prime stock is poised to soar higher.

Second Pick: Amazon

Amazon (NASDAQ: AMZN) holds sway in two sectors anticipated to undergo double-digit expansion during this decade: e-commerce and cloud computing. The company is well-positioned to sustain its dominance, owing to strategic maneuvers undertaken over the past few years. Rigorous challenges in 2022, culminating in Amazon recording its first annual loss in nearly a decade, instigated these maneuvers.

Mounting inflation applied pressure on Amazon’s expenditure and its patrons’ wallets. Consequently, Amazon embarked on an overhaul of its cost structure, transforming itself into a robust entity capable not only of recuperating from arduous conditions but also thriving in more favorable times.

Amazon devoted efforts toward enhancing efficiency across its fulfillment network, investing in high-growth spheres, and supporting its Amazon Web Services (AWS) clients by proffering cost-effective tools during economic downturns. These endeavors have yielded fruit, with Amazon transitioning from billion-dollar cash outflows and declines in operating income to a state of growth. In the most recent quarter, operating income quadrupled, and the company reported free cash flow exceeding $21 billion.

Moving forward, Amazon’s transition from a national to regional fulfillment model could persistently pare down costs and augment revenue. By dispatching parcels from facilities closer to consumers’ residences, Amazon incurs reduced logistical expenses and ensures prompt delivery. Moreover, Amazon is introducing an ad-supported tier to its Prime Video offering, a strategic move likely to yield billions in additional revenue, according to analysts’ forecasts.

As for AWS, Amazon’s commitment to artificial intelligence (AI) could propel the company to the vanguard of the forthcoming AI revolution. This is particularly significant considering that AWS has historically been a profit driver for Amazon.

Following an 80% upswing last year, Amazon, akin to Apple, is still teeming with potential for additional gains. Thus, if the Nasdaq adheres to its historical tendencies in 2024, this market titan is poised for another remarkable surge.

Should you invest $1,000 in Apple right now?

Prior to making an investment in Apple, consider this:

The Motley Fool Stock Advisor analyst team has just pinpointed what they perceive to be the 10 best stocks for investors to acquire at this moment… and Apple didn’t make the cut. The 10 chosen stocks have the potential to yield substantial returns in the forthcoming years.

Stock Advisor provides investors with a simple blueprint for success, including guidance on constructing a portfolio, regular updates from analysts, and two new stock picks each month. Since 2002, the Stock Advisor service has consistently surpassed the return of S&P 500 by more than threefold*.

*Stock Advisor returns as of January 16, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adria Cimino holds positions in Amazon. The Motley Fool has positions in and recommends Amazon and Apple. The Motley Fool adheres to a distinct disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.