Microsoft (NASDAQ: MSFT) recently hit a $3 trillion market cap, closing in on pioneering company Apple. Although the stock initially retreated following its stellar earnings report, it bounced back, signaling strong investor confidence.

Let’s delve into Microsoft’s earnings and valuation to assess its potential to break the $4 trillion market cap barrier.

Image source: Getty Images.

Microsoft’s Transformation

A decade ago, Microsoft Azure was in its infancy, and the cloud was not a significant part of the business. However, in the last ten years, the company has undergone a remarkable metamorphosis.

Historically, industry leaders have lost their dominance over time. Microsoft itself has a track record of appearing like a stalwart before making pivotal shifts. The recent surge in growth can be attributed to the company’s investments in cloud and artificial intelligence (AI).

In the second quarter of fiscal 2024, Intelligent Cloud recorded $25.88 billion in revenue with a 48.2% operating margin. The Productivity and Business Processes segment generated $19.25 billion in revenue with an impressive 53.4% margin, while More Personal Computing delivered $16.89 billion in revenue with a respectable 25.4% margin, considering its hardware focus.

The impact of AI on Microsoft is widespread. The company has experienced robust adoption of AI solutions, such as Microsoft Copilots in Office products, Microsoft Edge, and GitHub. For instance, GitHub Copilot’s paid subscribers reached 1.3 million, representing a 30% increase from Q1 fiscal 2024 and contributing to a 40% year-over-year rise in GitHub revenue.

Microsoft already boasts 53,000 clients for Azure AI. Notably, over half of the Fortune 500 companies utilize Azure OpenAI. During the earnings call, “AI” was a heavily emphasized term, signifying the company’s substantial commitment to AI and its tangible impact on the business.

Record-Breaking Quarter

An analysis of Microsoft’s Q2 results over the last decade vividly illustrates the company’s remarkable evolution.

Over the past five years, revenue has nearly doubled, while operating income and diluted earnings per share (EPS) have almost tripled due to margin expansion and stock repurchases. Comparatively, Microsoft’s current quarterly diluted EPS surpasses the yearly EPS figures from seven to ten years ago.

|

Metric |

Q2 FY15 |

Q2 FY16 |

Q2 FY17 |

Q2 FY18 |

Q2 FY19 |

Q2 FY20 |

Q2 FY21 |

Q2 FY22 |

Q2 FY23 |

Q2 FY24 |

|---|---|---|---|---|---|---|---|---|---|---|

|

Revenue |

$26.47 billion |

$23.8 billion |

$25.83 billion |

$28.92 billion |

$32.47 billion |

$36.91 billion |

$43.08 billion |

$51.73 billion |

$52.75 billion |

$62.02 billion |

|

Operating Income |

$8.02 billion |

$6.03 billion |

$7.91 billion |

$8.68 billion |

$10.26 billion |

$13.89 billion |

$17.90 billion |

$22.25 billion |

$20.4 billion |

$27.03 billion |

|

Operating Margin |

30.3% |

25.3% |

30.6% |

30% |

31.6% |

37.6% |

41.6% |

43% |

38.7% |

43.6% |

|

Net Income |

$5.86 billion |

$6.03 billion |

$6.27 billion |

($6.3 billion) |

$10.26 billion |

$11.65 billion |

$15.46 billion |

$18.77 billion |

$16.43 billion |

$21.87 billion |

|

Diluted EPS |

$0.71 |

$0.62 |

$0.80 |

($0.82) |

$1.08 |

$1.51 |

$2.03 |

$2.48 |

$2.20 |

$2.93 |

Data sources: Microsoft, YCharts.

One of the most fascinating aspects of Microsoft’s performance is its ability to simultaneously grow revenue and margins. AI plays a pivotal role in this achievement. In the latest quarter, 72.8% of Microsoft’s revenue was derived from the ultrahigh margin Productivity and Business Processes and Intelligent Cloud segments. The company’s strategic shift towards high-margin segments has propelled the overall operating margin to 43.6%, a significant leap from the pre-fiscal 2020 margin of around 30%.

Microsoft’s Prime Challenge

The primary concern for potential investors in Microsoft is its valuation.

Microsoft’s Path to a $4 Trillion Valuation

The Market’s Sentiment on Microsoft

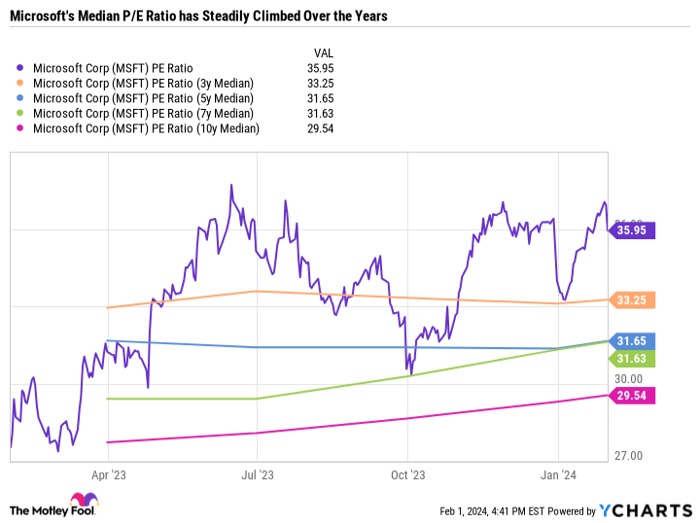

Microsoft is currently trading well above its historic multiple, as indicated by the chart above. It’s intriguing to note that the market has consistently attributed a higher multiple to Microsoft over time. The 3-year median price-to-earnings (P/E) ratio surpasses the 5-year, which, in turn, is higher than the 7-year, and so forth. This trend signifies that as Microsoft has evolved into a faster-growing and higher-quality business, the market has been willing to pay a higher multiple for its earnings, a justifiable response if Microsoft maintains its robust growth rate, as demonstrated in the recent quarter.

Investment Prospects and Potential Growth

While Microsoft currently deserves its 36 P/E ratio, any further valuation expansion hinges on the improvement of its revenue growth or margins, a proposition that is bordering on the arduous. Yet, the crux lies in the fact that, even at its present level, Microsoft doesn’t have to gain a valuation expansion to be an excellent investment. The logic is elegantly straightforward.

Assuming fair valuation at present, the stock would theoretically appreciate at the same rate as earnings growth. This means if earnings grow by 25%, the stock would need to also rise by 25% to maintain the existing P/E ratio. If the stock price remains the same, the P/E would fall to around 27 based on the current P/E of 36. Therefore, as long as Microsoft continues to grow earnings, the stock price should rise, keeping the stock attractive for long-term investors.

Microsoft’s Path to a $4 Trillion Valuation

The most straightforward route for Microsoft to achieve a $4 trillion valuation would be for the market to bestow a 50 P/E on the stock, catapulting it to that astronomical figure in no time. However, realistic prospects lie in good old-fashioned fundamentals.

Even if Microsoft maintains its current P/E ratio and its earnings surge by 33%, it would exceed the $4 trillion mark. And supposing its P/E contracts to, say, 30 (near the 10-year median), a 65% earnings upswing would still propel the company’s worth past $4 trillion. Given the current growth trajectory, it is plausible that Microsoft could achieve such earnings expansion within the next three years.

Whether achieved effortlessly or through toil, Microsoft remains a sturdy investment prospect. Even with a prospective valuation compress and a deceleration in earnings growth, the company could still comfortably surpass the $4 trillion milestone in the medium term. Unlikely to transpire this year, it is feasible for Microsoft to ascend beyond a $4 trillion valuation by 2026 or 2027.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.