Despite seeing solid wireless subscriber growth, shares of Verizon Communications (NYSE: VZ) fell after the company posted yet another overall mixed report. Nonetheless, the stock is still up over 30% over the past year, although up just over 10% year to date.

Investors continue to be drawn to the stock for its robust dividend. The stock currently has a forward dividend yield of about 6.5%.

Let’s take dive into Verizon’s third-quarter results to see why the stock fell and whether now is a good time to buy the stock on the dip.

Solid wireless subscriber growth

Verizon continues to see strength in its important wireless business, where revenue grew 2.7% to $19.8 billion. It added 349,000 retail postpaid net additions in the quarter, including 239,000 retail postpaid phone net additions.

Broadband also continues to perform well, with total net additions of 389,000. It ended the quarter with 11.9 million total broadband subscribers, a 16% jump versus last year. Most of the subscriber additions continue to be fixed wireless, while it added 43,000 net Fios subscribers.

The end of the Affordable Connectivity Program (ACP), which helped subsidize internet services, continued to be a drag, with prepaid revenue down another $40 million sequentially. However, the company said excluding Safelink, which catered to this program, it added 80,000 prepaid customers, its first quarter of net additions since acquiring TracFone in 2021.

Verizon Business also continued to be a drag, with revenue falling 2.3% to $7.4 billion. The company continues to lose wireline subscribers in this segment.

Wireless equipment revenue, meanwhile, sank 8.1% to $5.3 billion.

Overall, Verizon’s revenue was flattish year over year at $33.3 billion, while its adjusted earnings per share (EPS) fell from $1.21 a year ago to $1.19. Its adjusted EPS came $0.01 above analyst forecasts, while revenue came up just short of the $33.4 billion consensus. Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) rose 2.5% to $12.5 billion.

Looking ahead, the company kept its full-year guidance. It forecast full-year wireless revenue growth of 2% to 3.5%. It expects adjusted EPS to be in the range of between $4.50 and $4.70, with adjusted EBITDA to grow between 1% to 3%.

Image source: Getty Images.

The dividend is well covered

Turning to Verizon’s dividend, it remains well covered and has plenty of room to grow. The company paid out $8.4 billion in dividends through the first nine months of the year, while it generated $14.5 billion in free cash flow. That’s good for a 1.7x coverage ratio and gives the company plenty of room to continue to grow its dividend.

Meanwhile, Verizon’s balance sheet is also in good shape. Its leverage ratio on unsecured debt (net unsecured debt/trailing-12-month adjusted EBITDA) remained at 2.5.

Now the company is planning to increase its level of capital expenditures (capex) next year to between $17.5 billion to $18.5 billion. That will be up from the $17 billion to $17.5 billion it intends to spend this year. Much of this will go toward building out its broadband business. The company also agreed earlier to acquire Frontier Communications for $20 billion. It will integrate its fiber network into Fios.

Verizon now plans to end 2025 with a leverage ratio on unsecured debt of between 2 to 2.25 times.

Is the price dip a buying opportunity?

While the stock fell on its earnings report, there was still a lot to like. Verizon continues to see solid postpaid wireless and broadband growth. Meanwhile, it continues to generate a ton of cash, which easily covers its dividend and allows it to lower its debt, make acquisitions like Frontier, and pursue broadband growth opportunities.

The end of the ACP program will remain a drag until Verizon laps it, while its legacy wireline business will also likely slowly continue to roll off. However, with new artificial intelligence-focused smartphones, such as the iPhone 16, the company should see a turnaround in its wireless device business in the coming quarters.

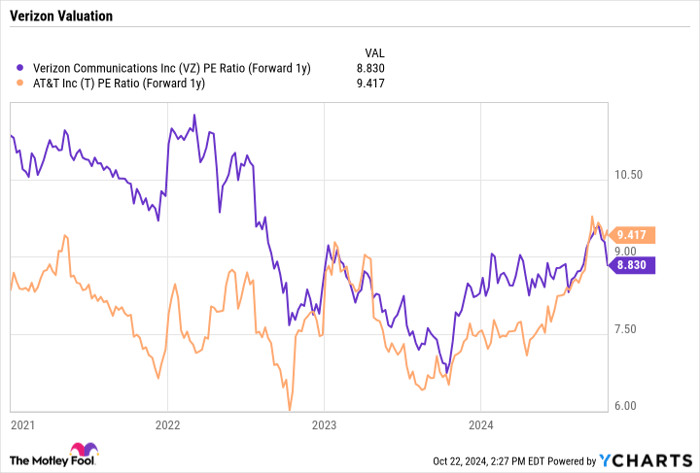

Looking at valuation, Verizon trades at just above a forward price-to-earnings (P/E) ratio of 8.8 based on 2025 earnings estimates, which is slightly below the multiple of AT&T. Typically, it has traded at a premium to its rival.

VZ PE Ratio (Forward 1y) data by YCharts

As such, I think the negative reaction to Verizon’s earnings is overdone. The company is still seeing its core businesses do well, while it has a robust dividend that is well covered and should continue to grow. As such, I’d be a buyer of the stock on the dip.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,154!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,777!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $406,992!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 21, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool recommends Verizon Communications. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.