Intel Corporation INTC has relinquished its coveted position on the Dow Jones Industrial Average (“DJIA”) — a leading stock market index of 30 blue-chip firms — to NVIDIA Corporation NVDA. The radical shakeup marks a significant shift in the semiconductor ecosystem with the growing dominance of AI (artificial intelligence) and ends Intel’s 25-year run in DJIA.

Moreover, the fact that Intel had the least influence on the index, owing to its lowest share price tally compared with the other Dow components, offered another compelling reason to dump the stock from the price-weighted index.

What Went Wrong for INTC?

Although Intel scaled its AI footprint with the launch of Core Ultra processors and Gaudi 3 accelerator featuring advanced graphics and AI processing power, it lagged NVIDIA on the innovation front with the latter’s H100 and Blackwell graphics processing units (GPUs) being runaway successes. Leading technology companies are reportedly piling up NVIDIA’s GPUs to build clusters of computers for their AI work leading to exponential revenue growth.

An accelerated ramp-up of AI PCs further affected the short-term margins of Intel as it shifted production to its high-volume facility in Ireland, where wafer costs are typically higher. Margins were also adversely impacted by higher charges related to non-core businesses, charges associated with unused capacity and an unfavorable product mix.

Intel has been facing challenges due to the disruptive rise of over-the-top service providers in this dynamic industry. Price-sensitive competition for customer retention in the core business is expected to intensify in the coming days. Aggressive competition is likely to limit the ability to attract and retain customers and affect operating and financial results.

Frigid US-China Trade Ties Hurt INTC

China accounted for more than 27% of Intel’s total revenues in 2023, making it the single largest market for the company. However, the communist nation’s purported move to replace U.S.-made chips with domestic alternatives significantly affected its revenue prospects. The recent directive to phase out foreign chips from key telecom networks by 2027 underscores Beijing’s accelerating efforts to reduce reliance on Western technology amid escalating U.S.-China tensions.

As Washington tightens restrictions on high-tech exports to China, Beijing has intensified its push for self-sufficiency in critical industries. This shift poses a dual challenge for Intel, as it faces potential market restrictions and increased competition from domestic chipmakers. The second-quarter 2024 revenues were adversely impacted by the revocation of certain licenses for exports of consumer-related items to a customer in China.

Moreover, weaker spending across consumer and enterprise markets, especially in China, resulted in elevated customer inventory levels, culminating in soft demand trends. Strict export control measures are further likely to affect the market dynamics.

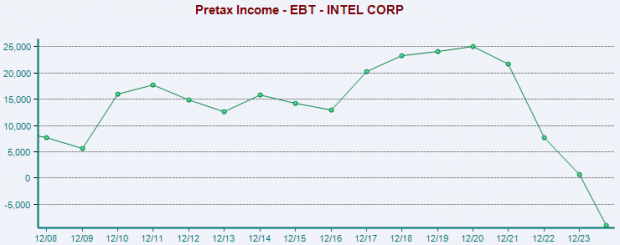

Image Source: Zacks Investment Research

INTC’s Price Performance

The stock has plunged 53.6% year to date against the industry’s growth of 123.6%, lagging its peers Advanced Micro Devices, Inc. AMD and NVIDIA. Much of this underperformance is due to severe financial difficulties and operational challenges, which have forced management to undertake a comprehensive review of its businesses.

Intel is mulling various options, including the potential split of its product design and manufacturing divisions and evaluating which factory projects should be terminated. It also plans to establish Intel Foundry as an independent subsidiary to unlock strategic benefits and improve capital efficiency with clearer separation and independence from the rest of Intel. The division incurred an operating loss of $5.8 billion in the last reported quarter.

YTD Price Performance

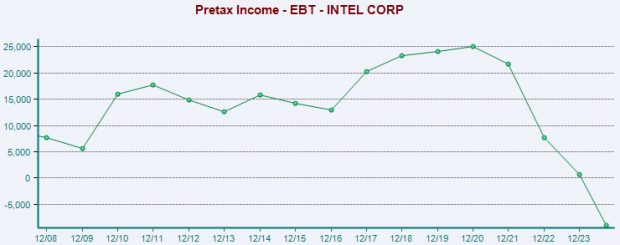

Image Source: Zacks Investment Research

Estimate Revision Trend of INTC

Earnings estimates for Intel for 2024 have moved down 87.8% to 23 cents over the past year, while the same for 2025 has declined 54.2% to $1.03. The negative estimate revision depicts bearish sentiments for the stock.

Image Source: Zacks Investment Research

End Note

Intel’s innovative AI solutions hold immense promise for the broader semiconductor ecosystem. By addressing the challenges of scalability, performance and interoperability, it is paving the way for widespread AI adoption across enterprises worldwide. Intel has retrenched a massive workforce during the last reported quarter and remains on track for more than a 15% workforce reduction before the end of the year. The company has reduced its capital expenditures by 20% since the beginning of the year and is focusing on simplifying parts of its portfolio to unlock efficiencies and create value.

However, with a Zacks Rank #4 (Sell), it appears that recent product launches are “too little too late” for Intel. In addition, margin woes amid strict export restrictions, unfavorable product mix and elevated customer inventory levels weigh on its bottom line. With declining earnings estimates and abysmal price performance compared with its peers, the stock is witnessing a negative investor perception. Consequently, it might be prudent to avoid the stock at the moment.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

It’s only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it’s positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>

Intel Corporation (INTC) : Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.