While Apple (NASDAQ: AAPL) may be the world’s largest company (a title that can switch between it and Nvidia on any given trading day), it isn’t without its investment risks. Apple isn’t the growth or the value investment it used to be; it’s just expensive now, with slow growth (or no growth in some areas).

If you’re an Apple investor, there are three big warning signs the company just displayed in its latest earnings report that you need to note. While these may not entirely break Apple’s investment thesis, they could affect the stock’s price movement.

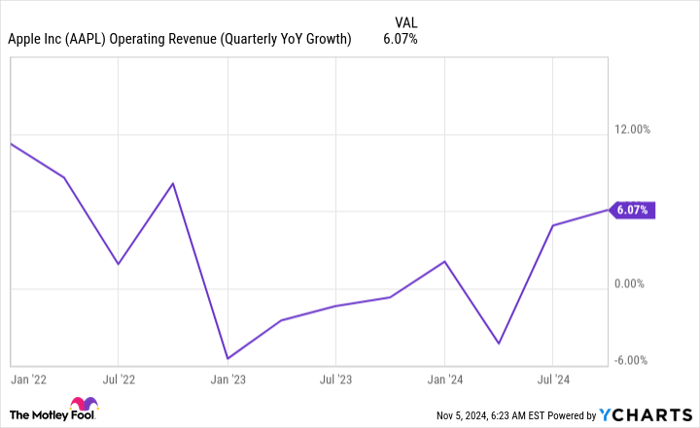

1. Apple hasn’t grown much in recent quarters

If I started this article by saying, “Apple’s Q4 FY 2024 (ended Sept. 28) had the fastest revenue growth in a quarter in two years,” you might be misled to think that it was a blowout quarter for Apple. However, that’s far from the case, as Apple’s revenue growth has been practically nonexistent since the start of 2022.

AAPL Operating Revenue (Quarterly YoY Growth) data by YCharts

Yes, 6% revenue growth isn’t very much and is the slowest growth rate of the “Magnificent Seven” stocks. However, this quarter wasn’t supposed to be a slow growth quarter, as it was hoped that the iPhone 16 would boost sales due to its new artificial intelligence (AI) feature set.

Unfortunately for Apple, iPhone sales only rose 5.5% year over year. Investors will need to wait until after Apple reports Q1 FY 2025 results (which encompasses the holiday quarter) to determine if the iPhone 16 was a flop, but as of right now, it doesn’t look good.

Apple’s revenue growth is not very rapid, but since Apple is a mature business, investors care more about profit growth than revenue. However, that area doesn’t look good, either.

2. Apple’s earnings growth isn’t much faster

Prior to this quarter, Apple had managed to put up respectable earnings growth, even if its revenue wasn’t growing quickly or shrinking in any given quarter. However, this quarter was a disaster from an earnings standpoint, as they fell from $1.47 last year to $0.97 this year — a 34% decrease.

While earnings per share (EPS) is useful, one-time events can heavily influence it. For example, Apple’s income tax provision rose from $4 billion last year to $14.9 billion this year. That jump was a one-time, $10.2 billion event caused by the reversal of the European General Court’s State Aid decision. Without that, management stated that its EPS would have been $1.64, good for a 12% rise.

That would indicate that Apple could put up market-beating earnings growth, since the stock market, measured by the S&P 500 (SNPINDEX: ^GSPC), usually grows about 10% per year. However, this is still something investors need to watch.

Apple is barely meeting the growth threshold a stock needs to beat the market year in and year out, so it would make sense for the stock to trade around an S&P 500 multiple. But that isn’t the case.

3. Apple’s stock is very expensive

From a valuation standpoint, Apple is very expensive. Because Apple has that one-time effect hit its earnings this quarter, the trailing price-to-earnings (P/E) ratio becomes useless. Instead, investors should look at the forward P/E ratio, as it shows where Apple is heading if it hits analyst projections.

AAPL PE Ratio (Forward) data by YCharts

At 30 times forward earnings, Apple isn’t a cheap stock. Compared to the S&P 500, which trades at 23.8 times forward earnings, Apple has a significant premium to the market despite growing around the same rate.

This isn’t a great combination, and unless Apple’s revenue and earnings growth accelerate, the stock could face a difficult road ahead.

As a result, I think investors should look elsewhere before investing in Apple. There are other businesses (like Alphabet) that trade for less than the S&P 500’s valuation and are growing much faster than Apple. These make for much more promising long-term investments and will likely outperform Apple over the long term — unless Apple can reaccelerate its growth.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $23,657!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,034!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $429,567!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 4, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, and Nvidia. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.