The Growth of Ad-Supported Memberships

When Netflix (NASDAQ: NFLX) unveiled its second-quarter results, the surge in ad-supported memberships acted as a beacon, guiding investors through the financial waters. Despite the somewhat lackluster response from the market, the stock stands proudly tall with a 33% yearly increase.

Delving into the streaming industry titan’s Q2 performance reveals a 16.8% revenue leap to a stunning $9.6 billion. The revenue growth trajectory has been on a steady rise over the last year, as illustrated in the table below.

| Metric | Q2 2023 | Q3 2023 | Q4 2023 | Q1 2024 | Q2 2024 |

|---|---|---|---|---|---|

| Revenue growth | 2.7% | 7.8% | 12.5% | 14.8% | 16.8% |

Earnings per share (EPS) didn’t shy away either, escalating from $3.29 to a solid $4.88, marking a robust 48.3% climb.

Global streaming memberships painted an impressive picture with a 16.5% increase to 277.65 million members, while ad-supported memberships fired up a stellar 34% sequentially.

Netflix indicated that ad-supported memberships accounted for about 45% of sign-ups where available. The subscription costs $6.99 a month in the U.S., offering streaming on two devices concurrently along with download capabilities. The strategic phasing out of basic plans in certain regions, like the U.K. and Canada, has fueled the upward trajectory of ad-supported plans. Plans are afoot to replicate this plan in the U.S. and France.

The streaming giant aims to hit critical mass for advertisers in its ad-supported markets by 2025, although ad revenue won’t spearhead growth this year or the next. Nevertheless, advertising is envisioned as a long-term revenue and profit propellant. The introduction of new advertising mechanics, such as displaying ads when shows are paused, bode well for future prospects.

Netflix’s recent foray into live events within its platform is touted to be a push in the right direction, likely luring in more advertising dollars. Streaming two live NFL games on Christmas Day is just the beginning of a potentially lucrative avenue without solely being reliant on sports rights. Securing WWE’s Monday Night Raw for the U.S., Canada, U.K., and Latin America from 2025 onwards adds more firepower to Netflix’s arsenal in terms of content inventory for ads.

Noteworthy improvements in guidance see Netflix upping the ante on both full-year revenue and operating margin forecasts. With revenue growth expected to hit between 14% and 15% this year, up from a previous range of 13% to 15%, the operating margin projection also saw a bump to 26% from 25%. A free cash flow target of approximately $6 billion for this year remains on the horizon.

The third quarter estimates feature revenue growth of nearly 14% to $9.7 billion and an anticipated EPS of $5.10.

Image source: Getty Images.

Prospects for Investing in Netflix Stock

Netflix’s Q2 triumph underscores the enduring vigor of the company’s operations, as it ushered in a swell of new memberships across its varied regions. In the foreseeable future, expect the company to embark on a trajectory toward a more hybrid model as advertising takes center stage in its endeavors.

This marks a significant turning point for the company, armed with a massive viewership base poised to attract advertisers seeking streaming audiences. The avenue for growth isn’t solely limited to ad-tier plans but extends to ad-supported live events and the potential introduction of less intrusive ads, strategically placed on landing screens or during show interruptions.

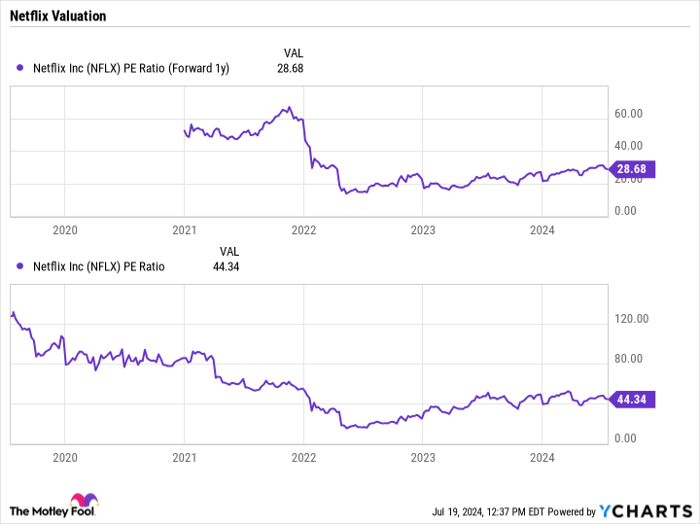

Trading at a forward price-to-earnings (P/E) ratio of under 29 times based on 2025 analyst estimates, Netflix’s stock appears favorably positioned given its historical P/E trends that have often surpassed 40 times.

NFLX PE Ratio (Forward 1y) data by YCharts

Given the imminent landscape of advertising opportunities over the next years paired with the current valuation, the allure of investing in Netflix shares appears compelling. While ad revenues may not steer the ship this year or the next, they are anticipated to be the driving force behind growth in the ensuing years.

Considering an Investment in Netflix

Prior to diving into Netflix stock, it’s prudent to reflect on this:

The Motley Fool Stock Advisor team recently spotlighted what they believe to be the 10 best stocks for investors currently… with Netflix passing the selection criteria. These chosen stocks bear the potential for monumental returns in the forthcoming years.

Recalling Nvidia’s illustrious inclusion back on April 15, 2005, provides a telling example of monumental potential. A $1,000 investment during the recommendation period could have blossomed into a whopping $722,626!*

Through Stock Advisor, investors receive a well-laid roadmap for success, replete with portfolio construction guidance, regular analyst updates, and a bountiful stream of two new stock picks each month. Since 2002, the Stock Advisor service has outpaced the S&P 500 return by more than fourfold.*

Explore the 10 recommended stocks »

*Stock Advisor returns as of July 15, 2024