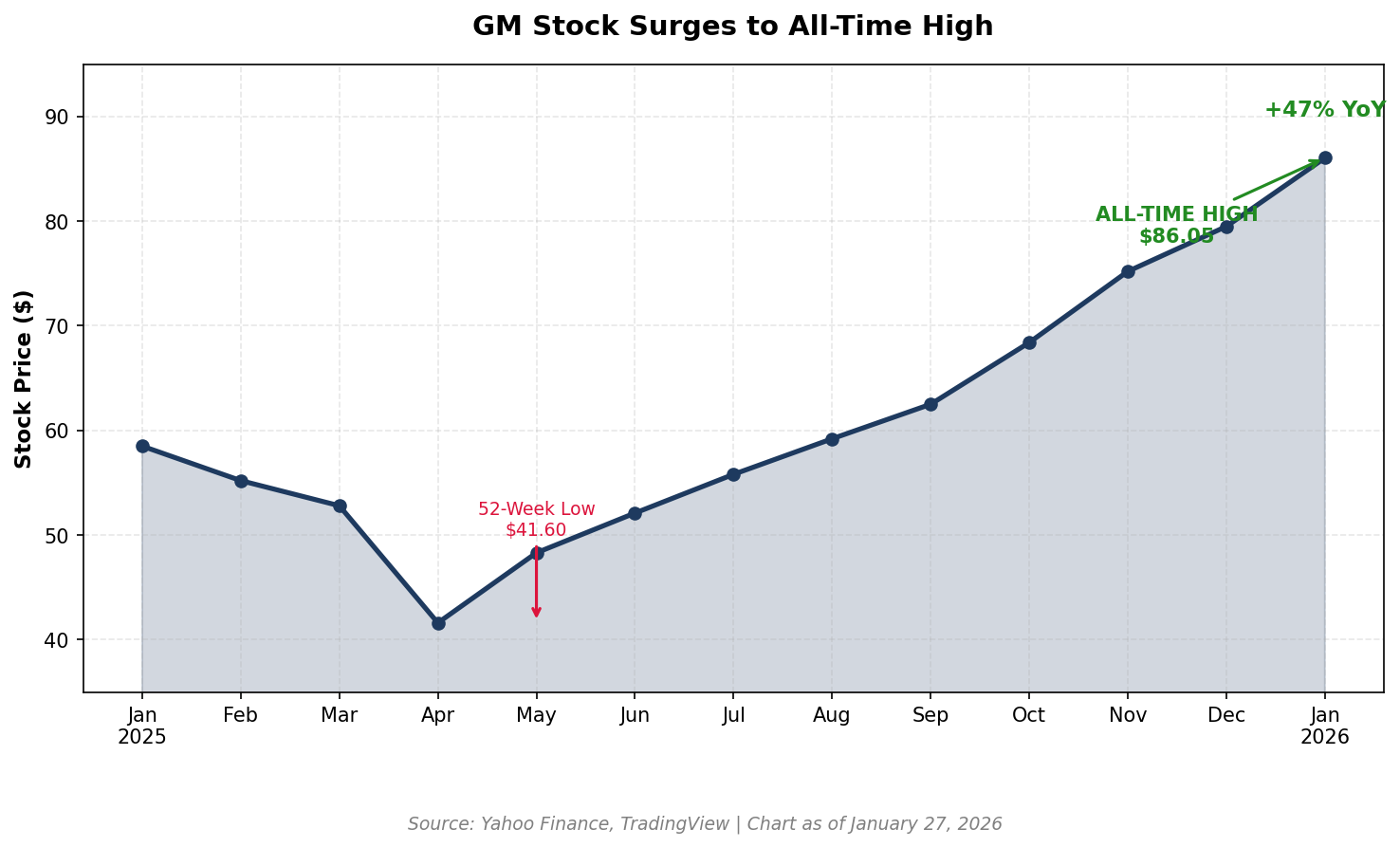

The automaker’s stock surged 9% on Tuesday to hit an all-time high of $86.05 after crushing earnings estimates and announcing a $6 billion share buyback alongside a 20% dividend increase. For a company that spent the past two years writing off billions in EV investments and dodging tariff bullets, the message is clear: ’s turnaround isn’t just working—it’s accelerating.

Shares are now up 47% over the past year. And if management’s guidance holds, the best may be yet to come.

")

The Numbers That Moved the Stock

Here’s what GM delivered for Q4 2025:

Earnings: Adjusted EPS of $2.51 vs. $2.28 expected — a 14% beat

Revenue: $45.29 billion vs. $45.37 billion expected — essentially in line

EBIT-Adjusted: $2.8 billion for the quarter; $12.7 billion for full year

Free Cash Flow: $10.6 billion for 2025

The headline numbers matter, but the shareholder returns announcement is what sent the stock to records. GM’s board declared a new $6 billion share repurchase authorization—the second such program in two years—and raised the quarterly dividend by 20% to $0.18 per share.

")

“The stock remains undervalued,” CFO Paul Jacobson said on the earnings call. With GM trading at roughly 7x forward earnings versus the S&P 500’s 22x, he’s got a point.

The 2026 Guidance: Why Analysts Are Bullish

GM issued 2026 guidance that exceeded Wall Street expectations on nearly every metric that matters:

|

Metric |

2026 Guidance |

2025 Actual |

|

Net Income |

$10.3B – $11.7B |

$2.7B |

|

EBIT-Adjusted |

$13B – $15B |

$12.7B |

|

EPS |

$11 – $13 |

$3.27 |

|

Adj. EPS |

$11 – $13 |

$10.60 |

|

North America Margin Target |

8-10% |

6.8% |

The jump from $2.7 billion in reported net income to $10+ billion guidance looks dramatic, but it’s misleading. 2025 included $7.2 billion in special charges from EV write-downs, restructuring costs, and China exits. Strip those out, and the underlying business has been recovering steadily.

The real story is margin recovery. GM’s North American EBIT margins collapsed from 9.2% in 2024 to 6.8% in 2025, crushed by $3.1 billion in tariff costs and elevated EV losses. Management is guiding for a return to 8-10% margins this year—a target that would add billions to the bottom line.")

The EV Pivot: Pain Now, Profits Later

GM took another $6 billion charge in January related to its electric vehicle business, citing softer-than-expected demand and the elimination of federal EV tax credits. Combined with previous write-downs, the company has now recognized over $8 billion in EV-related losses.

But here’s the contrarian take: this is exactly what GM needed to do.

By abandoning rigid EV production targets and pivoting to profitable hybrids and plug-ins, GM is finally matching supply to actual demand. CEO Mary Barra told CNBC the company expects EV unit losses to improve by $1 billion to $1.5 billion in 2026. That’s not a moonshot promise—it’s a realistic assessment of cost discipline catching up with the product line.

GM’s EV sales will likely run at just 5-7% of total volume this year, down from earlier projections. But the company’s full-size trucks, SUVs, and profitable ICE lineup continue to dominate their segments. Full-size pickup sales hit a 20-year high in 2025. Tahoe, Suburban, and Yukon led their categories for the fifth straight year.

The market is finally rewarding a realistic EV strategy over aspirational targets that never materialized.")

The Bull Case: Why This Rally Has Legs

1. Valuation remains absurdly cheap. At 7x forward earnings with a 47% one-year gain already in the books, GM still trades at a fraction of the broader market.

")

If margin recovery plays out, the stock could rerate significantly higher.

2. Capital returns are accelerating. Between the new $6 billion buyback and the dividend hike, GM is returning roughly 10% of its market cap to shareholders over the next 12-18 months. That’s a massive floor under the stock.

3. Tariff risk is manageable. GM guided for $3-4 billion in additional tariff costs in 2026, but that’s already baked into guidance. If Trump finalizes a South Korea trade deal with 15% tariffs (versus 25%), there’s upside to estimates.

4. The EV albatross is shrinking. Every quarter, EV losses improve. By 2027, management expects the segment to approach breakeven. That removes the biggest drag on reported earnings.

5. Analyst sentiment is turning. Goldman Sachs called it “a strong report” and noted GM expects 2026 to be better than 2025. UBS said the reaction should be favorable given “heightened investor concern around the quarter.” TD Cowen highlighted the free cash flow guide raise as “perhaps most impressive.”

The Risks: What Could Go Wrong

No turnaround is guaranteed. Here are the headwinds:

Tariff escalation: If Trump follows through on threats to raise South Korean auto tariffs to 25% (from the proposed 15%), GM’s 2026 guidance could be at risk. The company is the second-largest U.S. importer of Korean-made vehicles after Hyundai.

China deterioration: GM’s international operations—including the troubled China JV—remain a drag. The company is exiting unprofitable markets, but execution risk remains.

EV demand uncertainty: If EV adoption accelerates faster than expected, GM could find itself underinvested in the segment after years of write-downs.

Macro slowdown: Auto sales are cyclical. A recession would hit GM’s volumes and pricing power, regardless of cost discipline.

How to Play It

For investors looking to capitalize on GM’s turnaround, there are several approaches:

Direct equity: At 7x forward earnings with accelerating buybacks, GM offers value and income. The 20% dividend hike signals management confidence in sustainable cash flows.

Options plays: With implied volatility elevated post-earnings, selling puts on pullbacks could generate attractive premium while establishing a position at lower prices.

Sector basket: For broader auto exposure, consider pairing GM with and Stellantis (STLA), which face similar turnaround dynamics but at different stages.

The Bottom Line

General Motors just delivered everything investors wanted: an earnings beat, margin recovery guidance, a massive buyback, a dividend hike, and a path to EV profitability. The stock responded by hitting an all-time high.

The question now is whether this is the beginning of a sustained rerating or the peak of a cyclical rally. Given the valuation, capital returns, and improving fundamentals, the smart money is betting on the former.

Mary Barra has spent two years making hard choices—cutting EV ambitions, exiting China, absorbing tariff costs, and restructuring the business. Those choices are finally paying off. For patient investors, GM looks like one of the few genuine value plays left in this market.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.