Micron Technology, Inc. MU is all set to release its highly anticipated fiscal second-quarter 2026 results after the market closes on March 18. As in previous quarters, the report will provide key insight into memory chip demand, but is the stock a worthwhile investment now? Let’s take a closer look –

Micron’s Q2 Earnings in Sight: What’s on the Table

Micron is optimistic about its financial outlook and expects fiscal second-quarter 2026 revenues in the range of $18.3 billion and $19.1 billion, higher than fiscal first-quarter 2026’s $13.64 billion, according to investors.micron.com. The Zacks Consensus Estimate places Micron’s expected sales at $19.15 billion, implying 137.8% year-over-year growth. The company’s revenue growth trend remains strong, following a 57% year-over-year increase in the fiscal first quarter.

Revenues are expected to rise as robust dynamic random-access memory (DRAM) demand from data centers allows Micron to sell more units while also benefiting from higher prices in a tight memory market. Micron expects earnings per share (EPS) for the fiscal second-quarter 2026 to be $8.42, plus or minus 20 cents. The Zacks Consensus Estimate stands at $8.69 per share, indicating a 457.1% year-over-year increase.

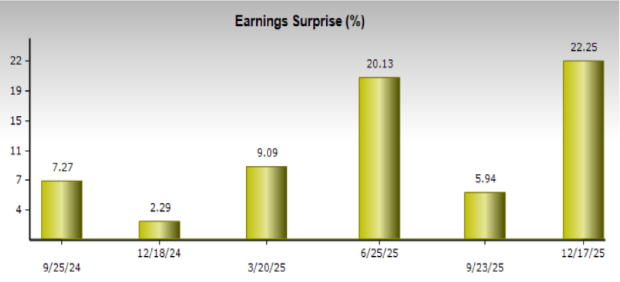

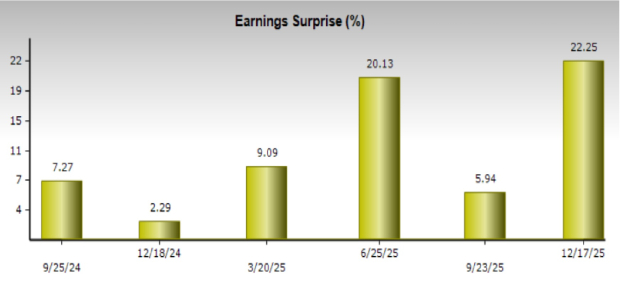

As a result, analysts anticipate Micron’s bottom line to grow more than fivefold. Additionally, Micron has delivered an average earnings surprise of 14.4% over the past four quarters, suggesting the company may post another strong performance in fiscal second-quarter 2026.

Image Source: Zacks Investment Research

Reasons to Be Bullish on Micron

Demand for Micron’s high-bandwidth memory (HBM) chips is expected to remain strong despite supply constraints, as they can handle large workloads while offering improved power efficiency. The demand for these chips remains resilient as data center operators and hyperscalers continue to ramp up AI infrastructure. Micron supplies HBM solutions to several tech players, including NVIDIA Corporation NVDA and Advanced Micro Devices, Inc. AMD, which compete in the graphics processing units market.

Micron has already sold out its available HBM chips for the current calendar year, and tight supply-demand conditions are expected to continue beyond this year. Sanjay Mehrotra, the CEO of Micron, believes that the demand-supply imbalance in HBM chips could push prices higher, which may benefit the company in the future.

Micron projects the HBM total addressable market to witness a CAGR of 40%, expanding from about $35 billion in 2025 to roughly $100 billion by 2028. Micron’s NAND flash chips are also expected to see a spike in prices due to tight supply until the middle of next year.

Buy, Hold, or Sell Micron Stock Ahead of Q2 Earnings

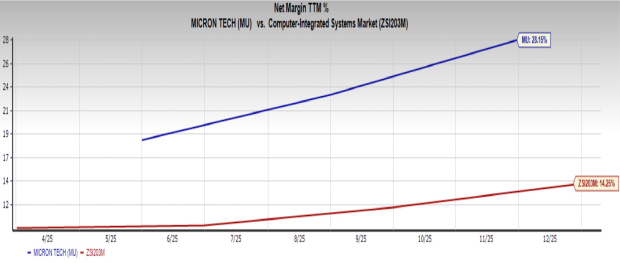

Micron projects strong fiscal second-quarter 2026 revenues and EPS growth driven by robust DRAM demand, which should boost its share price. Micron also expects strong demand and limited supply of its HBM and NAND chips, driving higher prices and fueling future growth. With a net profit margin of 28.2%, well above the Computer-Integrated Systems industry’s 14.3%, Micron demonstrates stronger profitability and growth potential.

Image Source: Zacks Investment Research

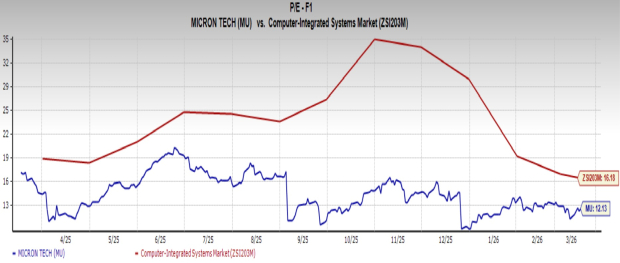

Therefore, savvy investors should capitalize on these strengths by investing in Micron stock now. Moreover, investors have the opportunity to buy Micron stock at a more favorable valuation than its industry peers, with a forward price/earnings ratio of 12.13, below the industry’s average of 16.18.

Image Source: Zacks Investment Research

Micron currently has a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks’ Research Chief Picks Stock Most Likely to “At Least Double”

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

Micron Technology, Inc. (MU) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.