Sohu.com Limited recently announced its fourth-quarter 2023 results, showcasing a mix of outcomes. The company surpassed the Zacks Consensus Estimate on the bottom line, but fell short on the revenue front. Despite notable efforts to enhance user engagement and pursue strategic investments, the leading provider of online advertising, media, and gaming services in China faced challenges with a year-over-year revenue decline. This downturn was largely attributed to the impact of stringent government regulations and prevailing macroeconomic headwinds.

Narrowing Losses in the Face of Headwinds

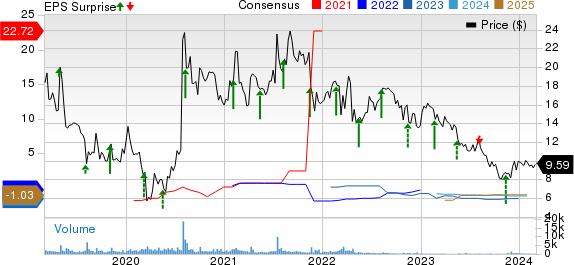

During the quarter, on a GAAP basis, Sohu reported a net loss of $12.6 million or 37 cents per American Depository Share (ADS). This represented an increase from the prior-year quarter, where the company reported a net loss of $7.1 million or 21 cents per ADS. The larger loss was primarily driven by a rise in operating expenses coupled with a decline in revenues.

The non-GAAP net loss for the quarter was $10.8 million or 32 cents per ADS, compared to a net loss of $2.2 million or 6 cents per ADS in the same period of the previous year. Notably, this figure was more favorable than the Zacks Consensus Estimate of a 40-cent loss.

Revenue Challenges and User Statistics

The reported quarter witnessed a decrease in revenues to $141.4 million, down from $160.4 million in the year-ago quarter. The decline in net sales within key business segments impacted the overall revenue performance. Brand advertising revenues fell by 30% year over year to $20.2 million, while revenues from Online Game dropped by 5% to $114.8 million. The decline was further exacerbated by reduction in portal, video, and real estate advertising revenues, as well as intensified competition in the online video market. Other revenues during the quarter were recorded at $6.5 million, contrasting with $10.3 million in the year-ago quarter.

When analyzing user engagement, for PC games, the total average monthly active user accounts (MAU) reached 2.3 million, indicating a 2% increase year over year. However, total quarterly aggregate active paying accounts (APA) dropped by 4% to 0.9 million. On the mobile games front, the total average MAU was 1.7 million, declining by 4% year over year. The total quarterly APA for mobile games fell by 14% to 0.3 million, primarily due to the launch of newer games overshadowing older titles.

Operational Insights and Financial Standing

Looking at key financial metrics, the gross profit for the quarter was $107.5 million, with a gross margin of 76%. The non-GAAP gross margin for brand advertising business dipped to 16% from 51% due to various factors such as the waiver of unpaid long-term accounts payable. Operating expenses on a non-GAAP basis rose by 3% year over year.

On the liquidity front, as of December 31, 2023, Sohu disclosed $362.5 million in cash and cash equivalents, along with $474.4 million in long-term tax liabilities. Comparatively, in the preceding year, the company held $697.8 million in cash and cash equivalents, with $448 million in long-term tax liabilities.

Future Projections and Market Context

In its outlook for the first quarter of 2024, Sohu anticipates Brand Advertising revenues to range between $15 million and $17 million, signaling a decline of 25% to 33% year over year. Online game revenues are estimated to fall within $110 million to $120 million, reflecting a decrease of 7% to 15% compared to the previous year. The company predicts a non-GAAP net loss between $23 million and $33 million, while GAAP net loss is expected to be in the range of $26 million to $36 million.

Industry Analysis and Stock Performance

Amid these developments, Sohu currently maintains a Zacks Rank #3 (Hold). While Sohu grapples with its financial performance, other industry players like NVIDIA Corporation and InterDigital, Inc. are experiencing their own market journeys. NVIDIA, a Zacks Rank #1 stock, has been showcasing impressive earnings surprises, benefiting from its focus on high-performance computing and AI solutions. On the other hand, InterDigital, with a Zacks Rank #2, has marked significant earnings surprises and excels in advanced mobile technologies.

Another notable player, Ubiquiti Inc., also carries a Zacks Rank #2 and is making a mark in the networking industry with disruptive pricing strategies and customer-centric product lines.