Finding undervalued artificial intelligence (AI) stocks isn’t easy. There is a lot of fluff in this space, as investors are excited about how game-changing this technology can be. However, there is one stock that I’d consider undervalued in this arena: Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL), the parent company of Google.

I’m not the only one who thinks that, either. Billionaire Steve Cohen and his hedge fund, Point72, purchased nearly a $200 million stake in Alphabet during the third quarter, a rather large bet that the stock is undervalued. So, why is Alphabet considered undervalued? It’s simple; it trades at a lower valuation than the S&P 500.

Alphabet is undervalued compared to the broader market

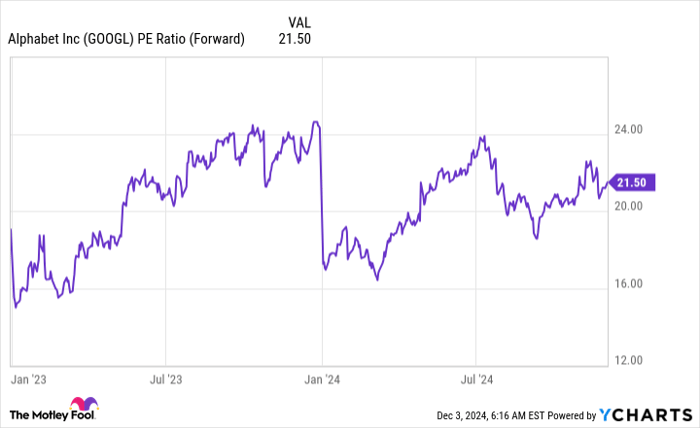

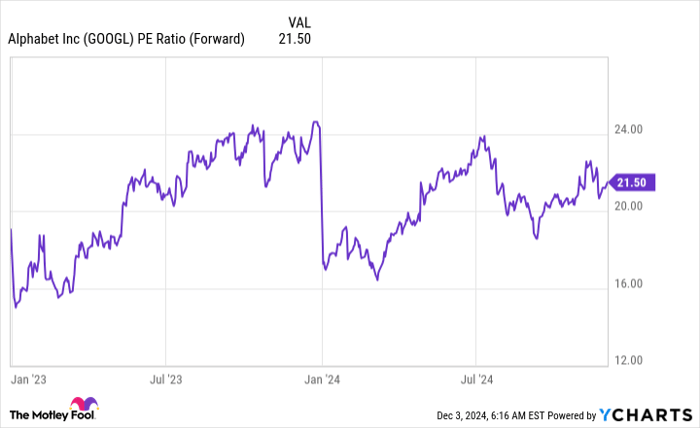

The S&P 500 is often used as a benchmark to measure companies because it is a broad market index. It gives a good average of all market sectors, even if it is most heavily weighted toward tech (which is by far the largest sector). Right now, the S&P 500 trades at a forward price-to-earnings (P/E) ratio of 23, which is a historically expensive figure. Alphabet trades for about 21.5 times forward earnings, thus its undervaluation moniker.

GOOGL PE Ratio (Forward) data by YCharts

But is it warranted?

Alphabet owns Google, which is the most used internet search platform by far. However, this dominance has gotten the company into trouble as the Department of Justice seeks to break up part of Google by forcing the sale of its Google Chrome browser. It’s unknown how large of an effect this would have on Alphabet, but it clearly would satisfy the DOJ’s wishes to strip Alphabet of its monopoly.

However, this is far from over. Alphabet will likely appeal the ruling, and the decision could last years until it potentially ends up in the Supreme Court. As a result, factoring this legal dispute into an Alphabet investment thesis becomes difficult. Furthermore, it also gives Alphabet time to build different channels so that it wouldn’t be as dependent on the browser to gather information. Because of this, I’m not factoring this DOJ decision into my investment thesis (which may be a mistake years down the road).

Alphabet is doing really well right now, and its best performing segment has nothing to do with the DOJ’s decision.

Google Cloud is a great reason to invest in Alphabet

In Q3, Alphabet’s revenue rose 15% year over year, and earnings per share (EPS) rose 37%. While advertising is Alphabet’s primary revenue driver (about three-fourths of revenue came from advertising), it only grew 10.4% in the quarter. That’s a ways off of its companywide 15% growth, so how did Alphabet’s revenue grow overall?

The rest of that growth came from my top reason for investing in Alphabet: Google Cloud. Google Cloud is Alphabet’s cloud computing wing — a platform that allows clients to rent computing resources from Alphabet. Google Cloud was doing well before the AI boom, but its growth has really accelerated recently. Google Cloud revenue rose 35% year over year, powered by new workloads coming online drawn by Alphabet’s strong AI infrastructure.

Google Cloud gives its clients access to the fastest Nvidia GPUs and Google’s custom tensor processing units (TPUs), which provide superior performance to GPUs when the workload is configured correctly. Additionally, Google’s in-house generative AI model, Gemini, is one of the top offerings in the space and is available to build on Google Cloud.

Don’t be surprised to see Google Cloud’s strength carry on throughout 2025, as it will become a massive part of its business. With a final DOJ resolution likely years away and Alphabet capitalizing on the AI arms race, it seems like a solid investment story. Throw in the fact that it’s valued at a lower level than the S&P 500, and it seems like a no-brainer investment.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $376,143!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,028!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $494,999!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 2, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet and Nvidia. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.